Written by

Eric

Share this article

.svg)

Subscribe to updates

I still remember a client who finally found their dream downtown apartment, only to have their heart broken weeks later. The mortgage application fell through because the building was labeled "non-warrantable." It was a devastating, expensive lesson.

From a homebuyer's perspective, whether a condo is warrantable or not essentially decides one crucial thing: can you get a standard mortgage to buy it? If you are house hunting right now, understanding this concept is vital. In this guide, I will walk you through exactly what a warrantable condo is, why it matters, and how to protect yourself from financing traps before you sign any contracts.

Also Read:

- Warrantable vs Non-Warrantable Condo: What's the Difference?

- [Read First] What is a Non-Warrantable Condo Loan?

- Best Non-Warrantable Condo Lenders Near Me in 2026

Key Takeaways

- The definition: It is a condo that meets the strict lending guidelines of major government-sponsored enterprises like Fannie Mae or Freddie Mac.

- The main benefit: Warrantability is the key to securing your mortgage. It allows you to get traditional financing with lower interest rates.

- The biggest red flags: Avoid "condotels," properties where one single entity owns too many units, or homeowner's associations (HOAs) facing active legal battles.

What is a Warrantable Condo?

In simple terms, a warrantable condo is a property that meets the financial and structural requirements set by Government-Sponsored Enterprises (GSEs) like Fannie Mae and Freddie Mac.

Why do we even use this specific term? It all comes down to financial risk. When you take out a conventional mortgage, your local bank usually doesn't keep that loan forever. They sell it to these massive institutions to free up capital. However, Fannie Mae will only buy the loan if the entire condo building, not just your individual unit, is deemed a safe investment. This is not a judgment on your kitchen's granite countertops. It is strictly a judgment on financial risk. If a building is warrantable, lenders feel secure giving you money.

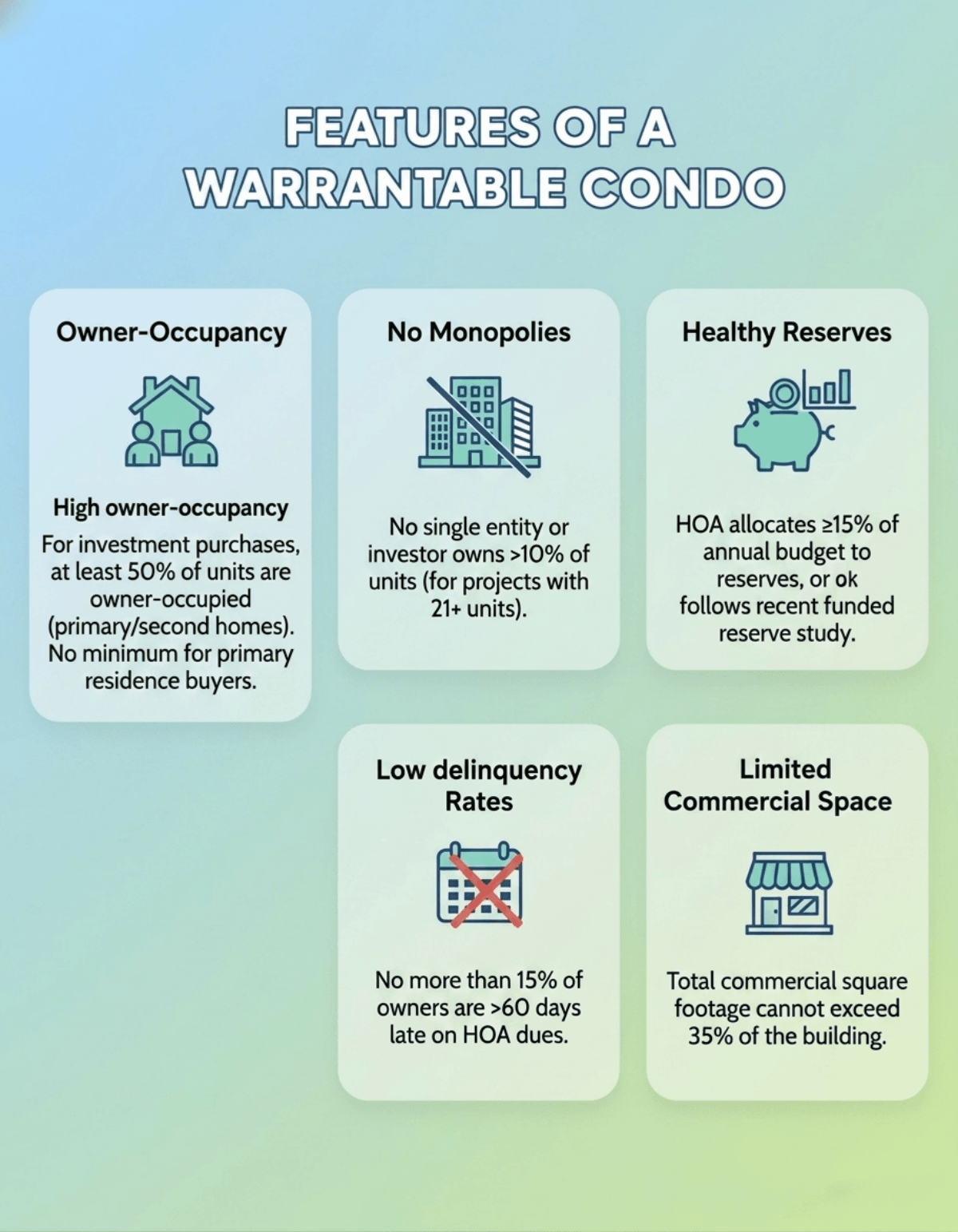

Features of a Warrantable Condo

So, what specific boxes must a building check to get this golden stamp of approval? The guidelines are rigid, but they exist to ensure the community is financially healthy.

Based on the current rules, here are the standard features a condo community must have to be considered warrantable:

- High owner-occupancy: For investment property purchases, at least 50% of units must be owner-occupied (primary residences or second homes). No minimum for primary residence buyers.

- No monopolies: No single entity or investor can own more than 10% of the units in a project with 21 or more units (Fannie Mae guideline).

- Healthy reserves: Healthy reserves: The HOA must allocate at least 15% of its annual budget to a replacement reserve fund, or follow a recent fully funded reserve study.

- Low delinquency rates: No more than 15% of the condo owners can be over 60 days late on paying their HOA dues.

- Limited commercial space: The building's commercial space, like ground-floor restaurants, cannot exceed 35% of the total square footage.

Why Warrantability Matters When Buying a Condo

You might wonder why you should care about the HOA's overall budget if you just want a nice place to live. The truth is, buying a warrantable condo directly impacts your wallet.

Here is why it matters so much:

- More Financing Options: You unlock the ability to use conventional loans and FHA loans, which make up the vast majority of the mortgage market.

- Lower Interest Rates: Because the risk to the bank is lower, you are rewarded with better interest rates and much friendlier down payment requirements.

- Higher Resale Value: Think about the future. When it is time for you to move, a warrantable unit is much easier to sell. Liquidity is high because your future buyer will not struggle to get a loan either, keeping the resale value strong.

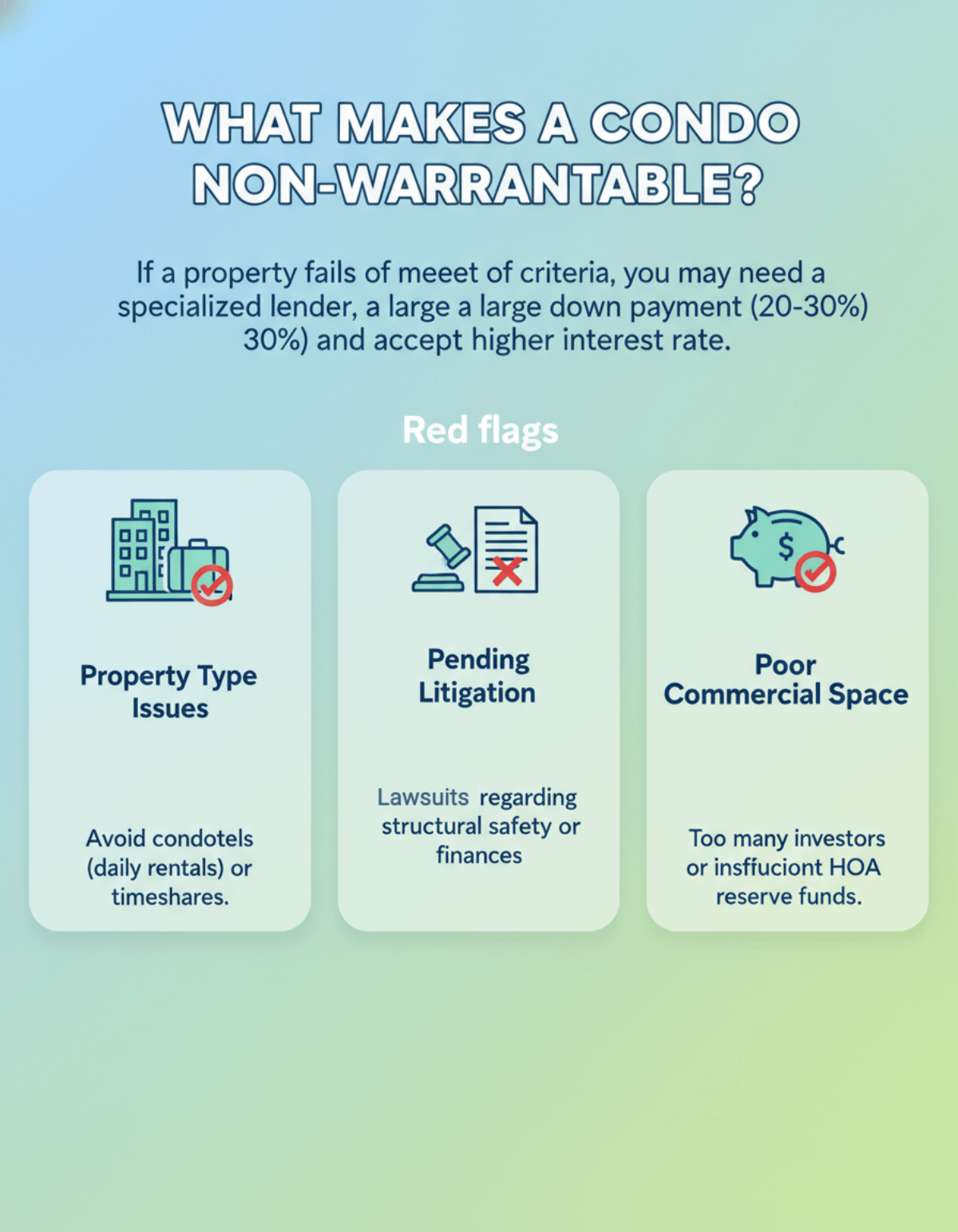

What Makes a Condo Non-Warrantable?

If a property fails to meet the criteria mentioned above, it falls into the non-warrantable category. While you can still buy these units, you will likely need to find a specialized portfolio lender, put down 20% to 30% in cash, and accept a much higher interest rate.

Watch out for these common red flags:

- Property type issues: Avoid condotels (condos operating like hotels with daily rentals) or timeshares. Banks hate short-term rental models.

- Pending Litigation: If the HOA is involved in a lawsuit regarding structural safety, habitability, or massive financial damages, lenders will hit the brakes immediately.

- Poor financials: A building flooded with investors, or an HOA lacking sufficient reserve funds, signals a high risk of bankruptcy.

How to Verify Whether It Is a Warrantable Condo?

As a buyer, you cannot tell if a building is warrantable just by touring the beautiful lobby. You need cold, hard paperwork.

Here is my step-by-step approach to verifying a property:

- Ask your real estate agent early: Before touring, ask them to check the MLS notes or call the listing agent to see if previous buyers successfully used conventional financing.

- Rely on the Condo Questionnaire: This is the ultimate deciding factor. Once you apply for a loan, your lender will send a highly detailed Condo Questionnaire to the HOA. Their answers will make or break your approval.

- Check official databases: If you plan to use an FHA loan, search the HUD website for their FHA-Approved Condo List (add external link here). It is a quick way to see if the building has already been vetted.

FAQs About a Warrantable Condo

Q1. Can I get a mortgage on a non-warrantable condo?

Yes, but you cannot use a standard Fannie Mae or FHA loan. You will need to find a specialized portfolio lender or utilize Non-QM loans. These alternative options usually require a steep 20% to 30% down payment and come with higher interest rates.

Q2. Do warrantable condos hold their value better?

Absolutely. Because they are easier to finance, the pool of potential buyers is much larger. This steady market demand helps maintain stable property values and ensures you won't be stuck with an unsellable asset in the future.

Q3. What is a condo questionnaire?

It is a comprehensive financial and operational survey that your mortgage lender sends to the condo's HOA. It asks detailed questions about the building's reserve funds, renter-to-owner ratio, commercial space, and legal history to determine warrantability.

Q4. How do pending lawsuits affect a condo's warrantability?

If the HOA is facing a lawsuit related to structural integrity, safety, or significant financial penalties, lenders will immediately flag the building as non-warrantable. They will not approve traditional loans until the legal issues are fully resolved.

Q5. Is it hard to sell a non-warrantable condo?

It is relatively difficult. Your buyer pool shrinks drastically because most people rely on conventional financing. You will mainly have to target all-cash buyers or those wealthy enough to afford high down payments, which often prolongs the selling process.

Conclusion

Ultimately, warrantability is a safety net. It protects both the bank and you, the buyer, from sinking money into a poorly managed or financially unstable building.

Based on my years of observing the real estate market, my strongest piece of advice is this: never assume a beautiful building is financially sound. Before you hand over your earnest money, always ensure your purchase contract includes a Financing Contingency. This crucial clause guarantees that if your lender discovers hidden HOA issues and deems the condo non-warrantable, you can walk away from the deal and get your deposit back without any penalties. Taking this one simple step will save you from sleepless nights and potential financial ruin.

People Also Read

- Bank Statement Mortgage Guidelines: What Is It? How to Verify?

- Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

- 8 Best Non-QM Mortgage Lenders: Which to Choose?