Written by

Eric

Share this article

.svg)

Subscribe to updates

Let's be honest: the mortgage origination process has always been notoriously complex, and it all starts with the dreaded 1003 form. I've seen borrowers pull their hair out over the endless paperwork, while loan professionals like myself used to lose countless hours just doing manual data entry.

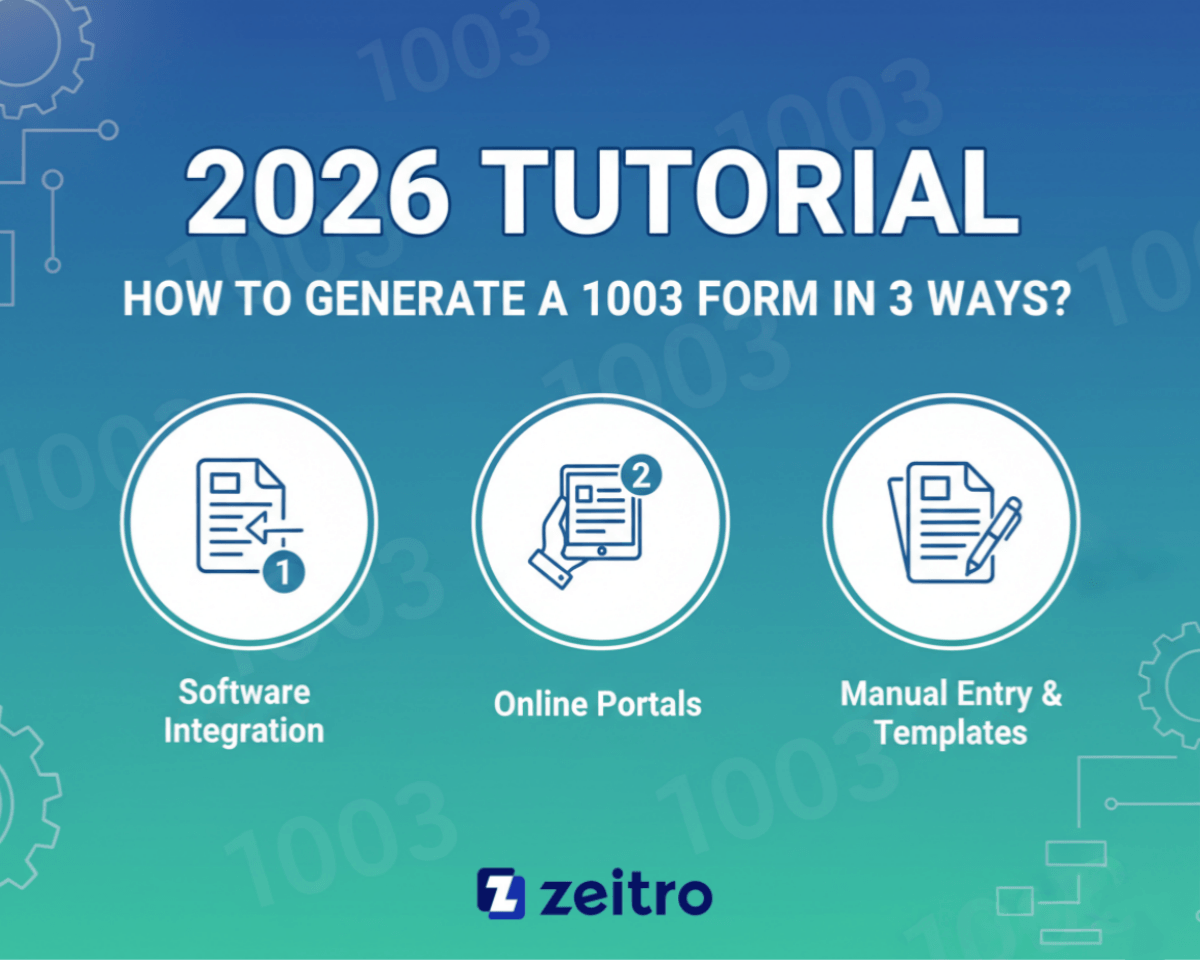

But it's 2026, and the days of tedious paperwork are fading. In this tutorial, I'll walk you through how to generate a 1003 form efficiently, shifting from outdated manual methods to the latest AI-driven automation that actually gets deals closed.

Key Takeaways

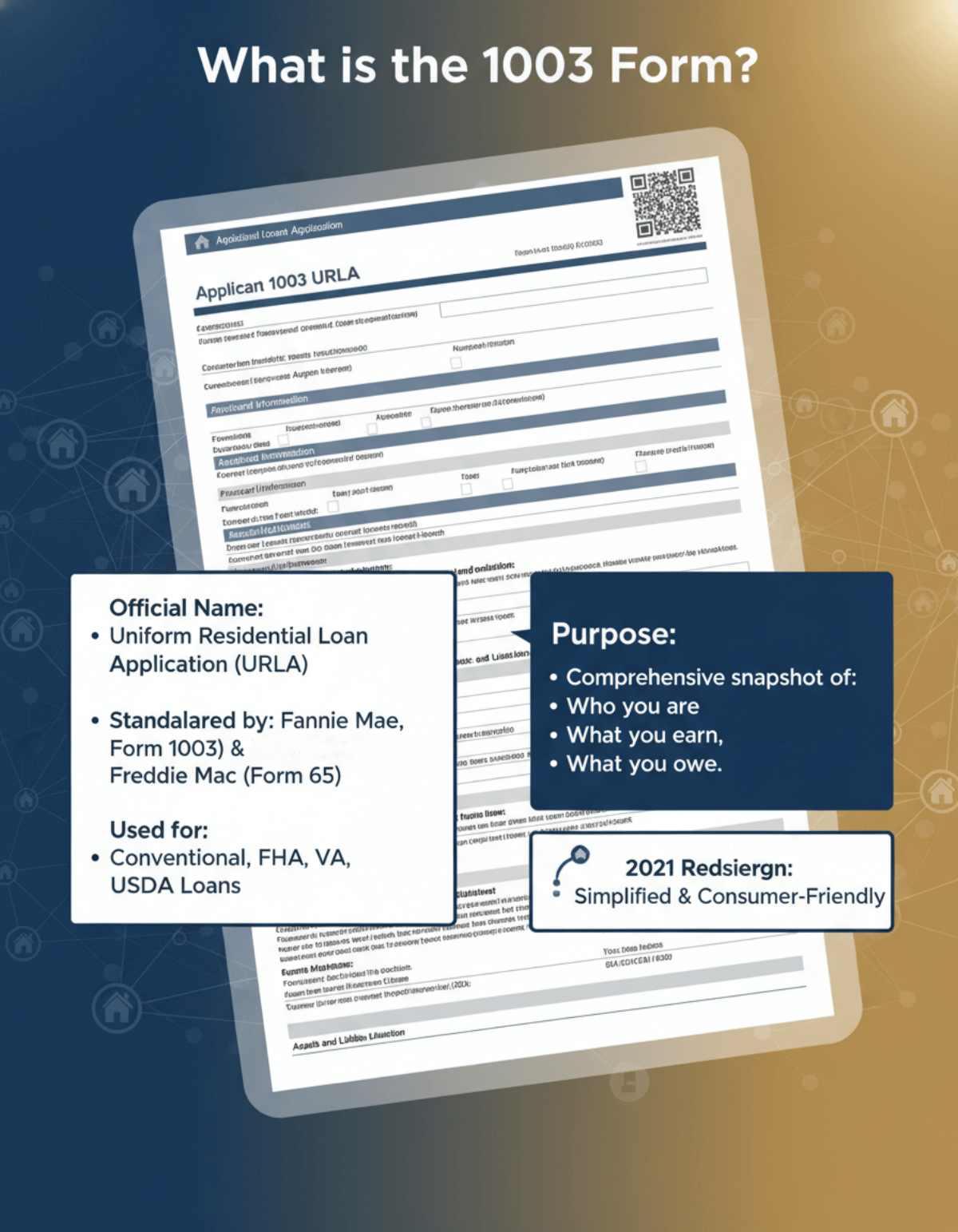

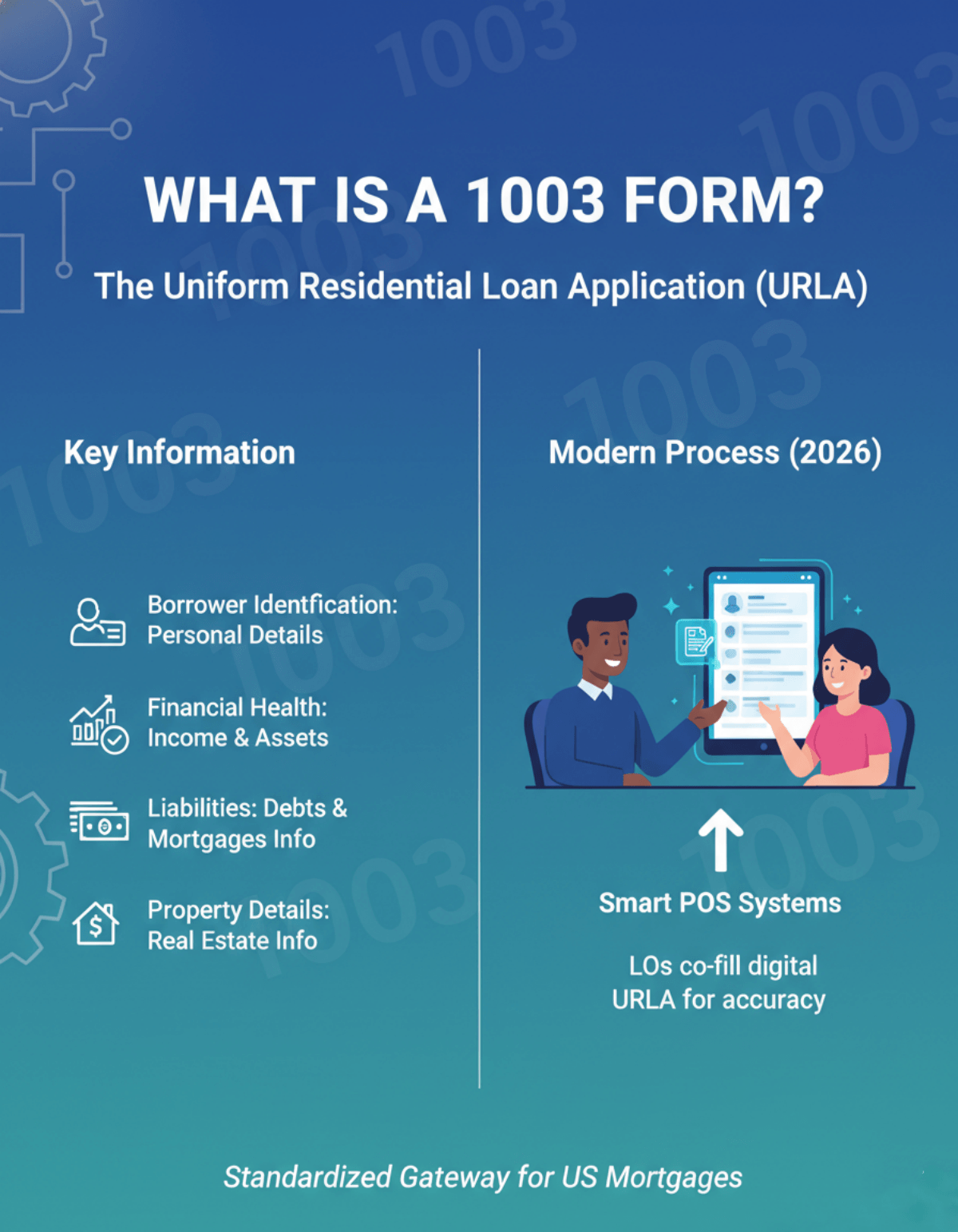

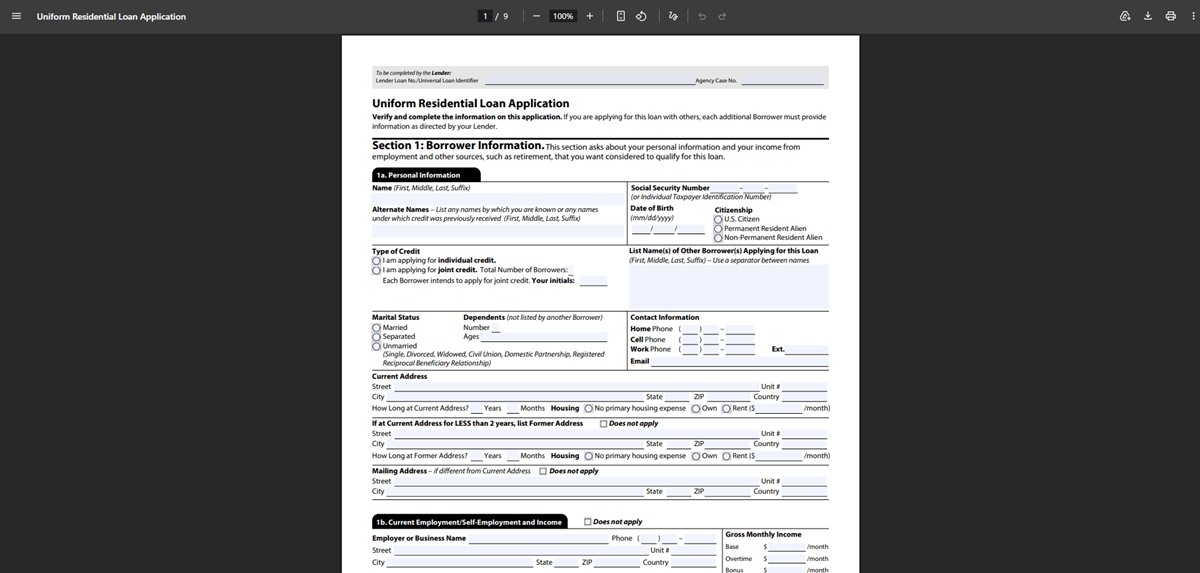

The 1003 Form, officially known as the Uniform Residential Loan Application (URLA), remains the absolute backbone of any modern mortgage application.

You can generate this document through three main avenues: AI-powered platforms, traditional lender portals, or manual PDF templates.

Adopting an AI-driven Point of Sale (POS) system like Zeitro is the 2026 industry standard, eliminating 100% of manual guideline work and empowering borrowers to finish the application in under 5 minutes.

What is a 1003 Form?

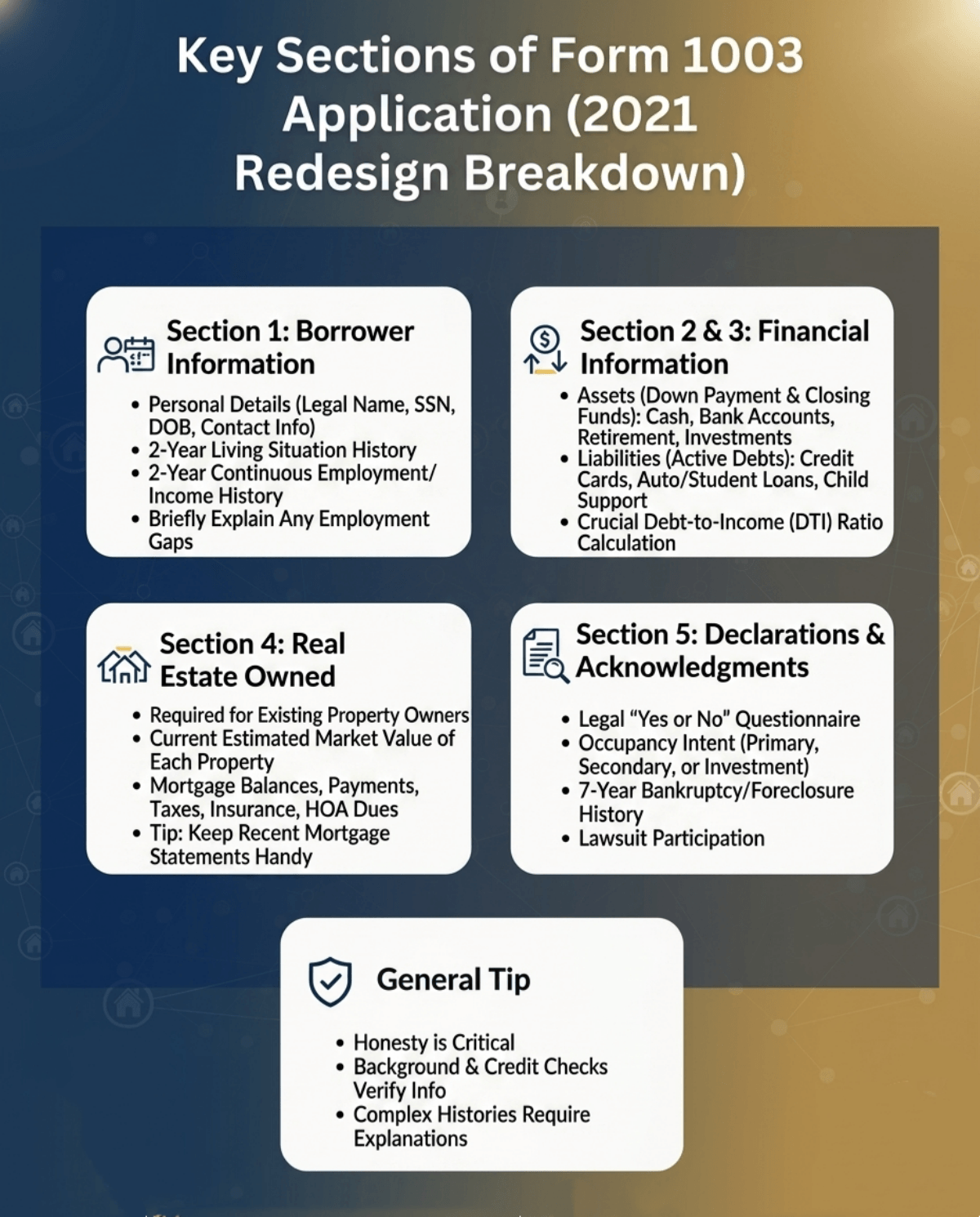

If you are new to the industry, you might be wondering what exactly this document is. The 1003 form is officially known as the Uniform Residential Loan Application (URLA). You will also hear it referred to as Freddie Mac Form 65—they are the exact same document. Fannie Mae originally developed it, and today, it is the standardized gateway for almost every residential mortgage in the United States.

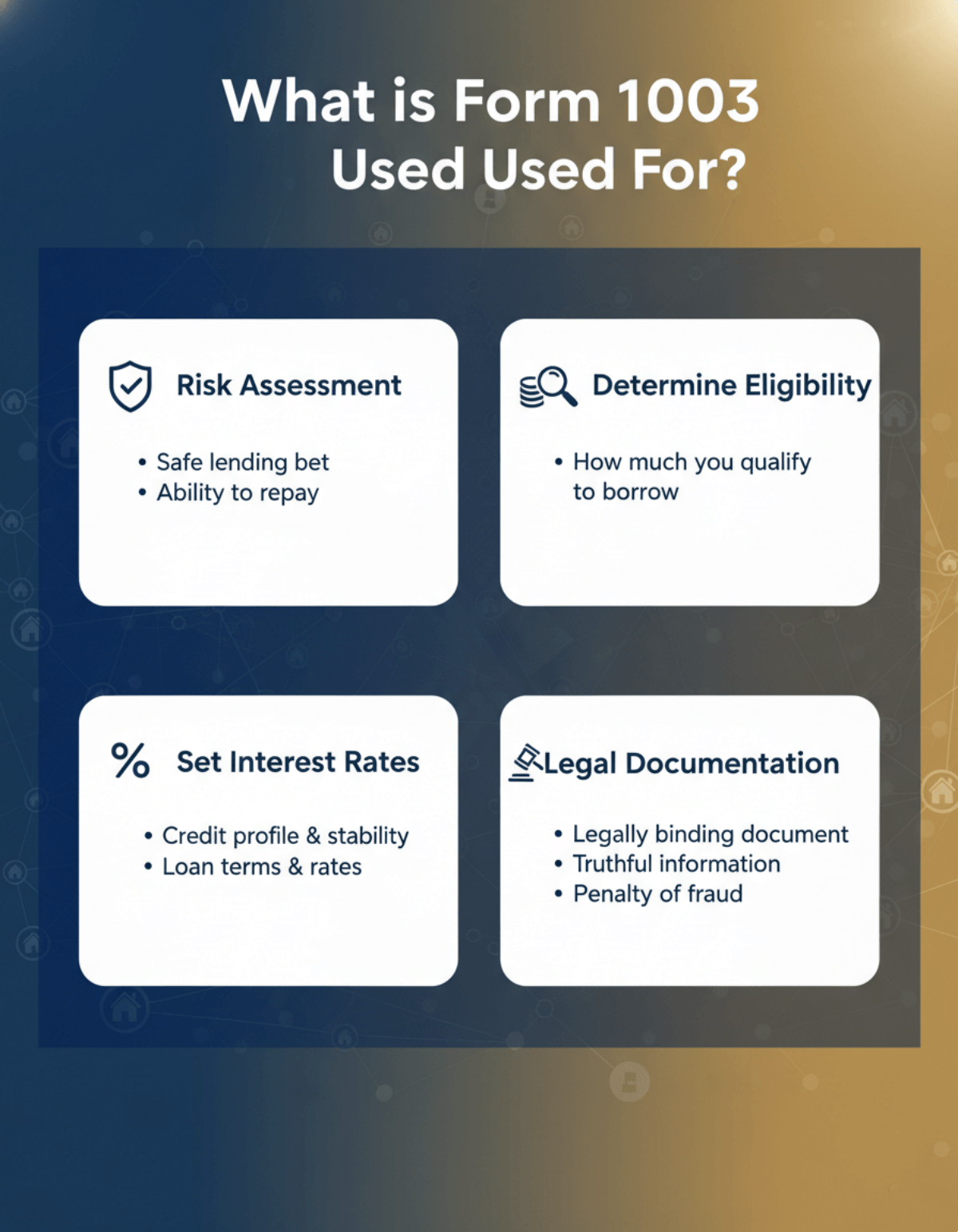

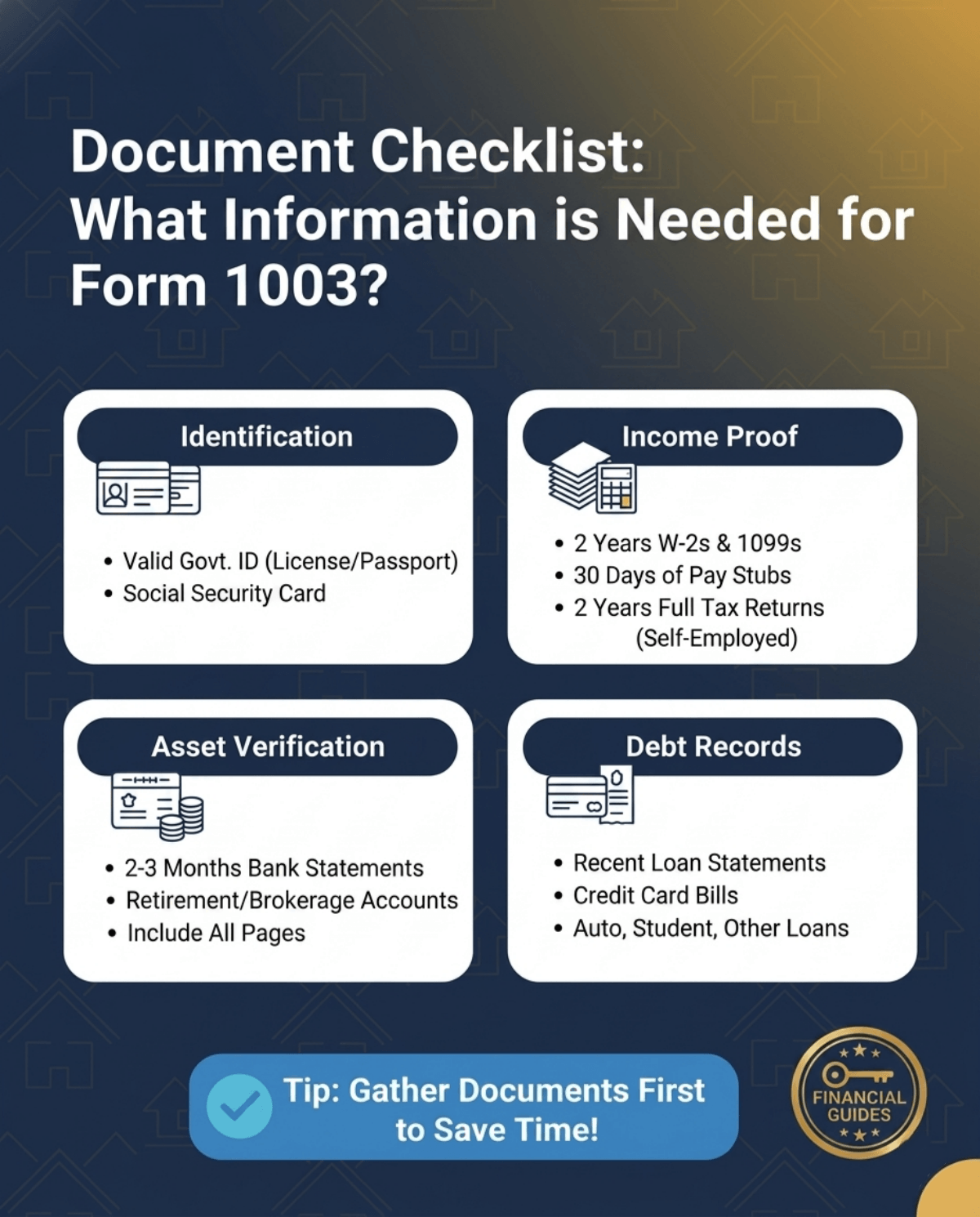

At its core, the 1003 form is designed to collect essential borrower data to determine creditworthiness. Its primary purposes include documenting:

- Borrower identification: Basic personal details and demographic information.

- Financial health: Comprehensive breakdowns of current income, employment history, and liquid assets.

- Liabilities: Existing debts, previous mortgages, and credit obligations.

- Property details: Information regarding the specific real estate being purchased or refinanced.

Who is Required to Fill out the 1003 Form?

Technically speaking, the borrower is responsible for providing the information and must sign the document to certify its absolute accuracy under penalty of perjury.

However, in 2026, I rarely see Loan Officers hand a borrower a blank URLA to figure out on their own. Instead, modern LOs utilize smart POS systems. We guide borrowers through an intuitive digital questionnaire, essentially co-filling the data to ensure 100% compliance and accuracy right out of the gate.

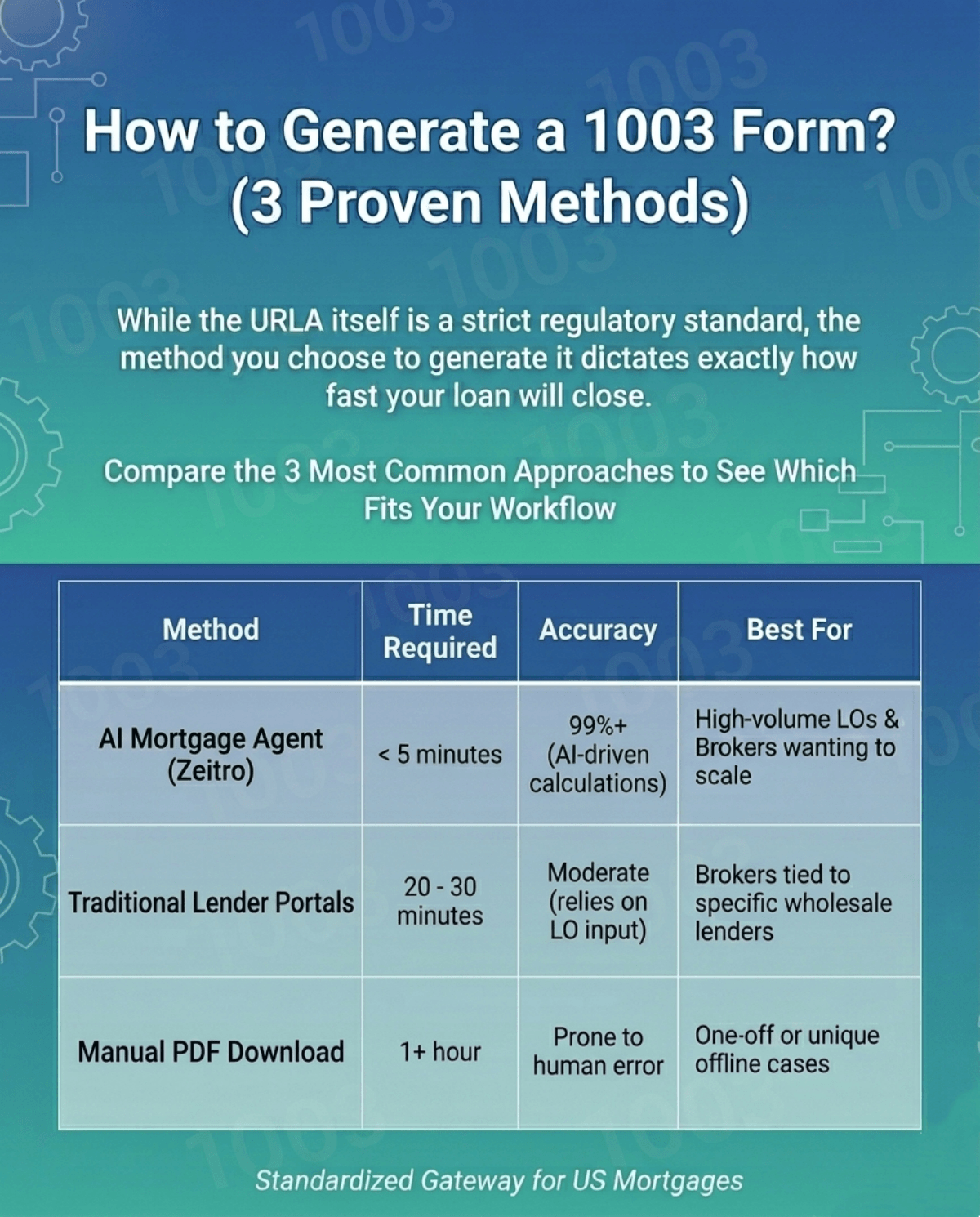

How to Generate a 1003 Form? (3 Proven Methods)

While the URLA itself is a strict regulatory standard, the method you choose to generate it dictates exactly how fast your loan will close. Let's break down the three most common approaches today to see which one fits your workflow.

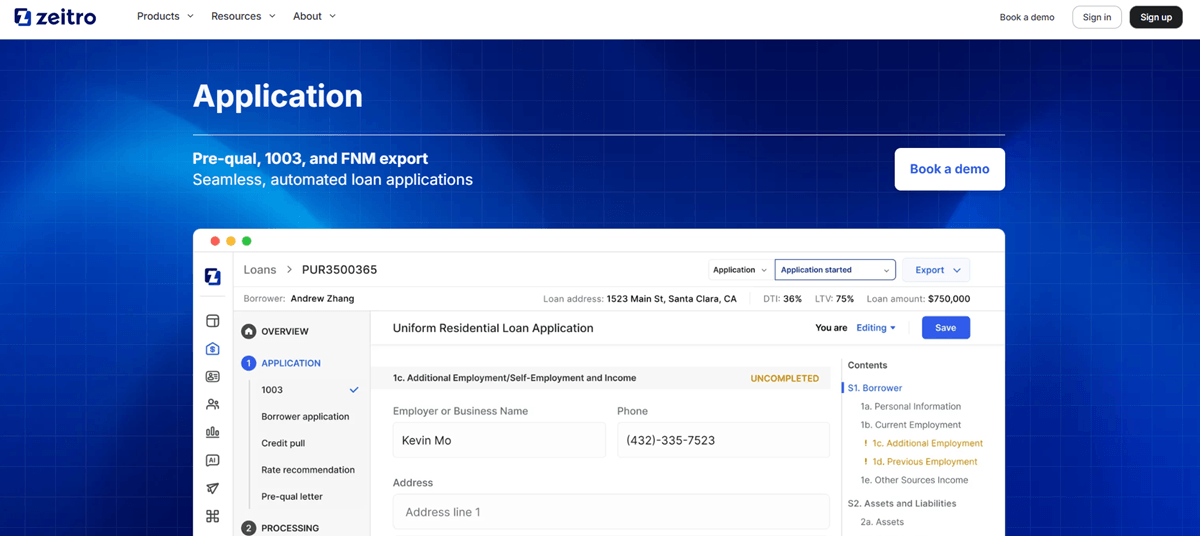

Method 1: Using an AI Mortgage Agent (Zeitro)

If you want to survive the highly competitive 2026 market, this is the ultimate solution. I personally transitioned to using an AI mortgage agent, specifically Zeitro's Application System, and it completely changed how my team operates. Zeitro is positioned as an intelligent platform specifically engineered for mortgage professionals, seamlessly integrating self-serve pre-qualifications, digital 1003 generation, and FNM 3.4 export.

Its core features are built around eliminating friction. The system provides real-time credit pulls and AI-driven instant Debt-to-Income (DTI) calculations. Because it supports everything from Fannie Mae and FHA to Non-QM and DSCR loans, it automatically formats borrower data into the standard FNM 3.4 file for seamless lender integration.

The business value here is undeniable. My borrowers achieve 90%+ application completion rates, finishing the process in just 5 minutes. Meanwhile, it saves Loan Officers over 20 hours per month. It achieves an 85%+ income calculation accuracy, reduces manual guideline lookups from 30 minutes to literal seconds, and eliminates 100% of manual guideline work. By streamlining this front-end mess, loan originators are closing 30% more loans.

Method 2: PDF Download and Manual Completion

For those who prefer the old-school route, you can still generate the form manually. You simply visit the official Fannie Mae website and download the interactive URLA PDF. From there, the process usually involves emailing the blank document to your borrower, having them print or type it out, and then painstakingly re-typing that exact same data into your Loan Origination System (LOS).

I have to warn you, though: this method is packed with massive drawbacks. Relying on manual data entry is highly prone to human error, which will inevitably cause underwriting delays. Furthermore, it completely lacks real-time DTI checks or automated credit pulls. In an era where consumers expect a seamless digital experience, sending them a daunting 9-page PDF essentially ruins the modern borrower experience and risks losing the deal altogether.

Method 3: Traditional Lender Portals & LOS

The middle-ground method that many brokers still use today involves generating the 1003 directly inside a Loan Origination System (LOS) or a wholesale lender's proprietary portal. Platforms provided by massive players like UWM or Rocket Pro TPO allow you to build out the application within their specific ecosystems.

While this is certainly a step up from emailing blank PDFs, there's a catch. It still frequently requires the loan officer to manually input the raw data they've collected from the borrower via endless phone calls or disjointed emails. These traditional portals lack the modern, intuitive "borrower self-serve" AI features found in systems like Zeitro. Consequently, you are still consuming a significant amount of your own valuable time playing data-entry clerk rather than actually advising your clients and originating new loans.

FAQs About Generating a 1003 Form

Q1. What is the FNM 3.4 format and why is it important for the 1003 form?

The FNM 3.4 format is the strict industry-standard data file required to securely import 1003 application data into lender systems. It ensures seamless compatibility, allowing loan officers to transfer a borrower's complete financial profile into an LOS without having to type anything manually.

Q2. Can borrowers complete a 1003 form entirely online?

Absolutely. While they used to fill out paper packets, modern POS systems like Zeitro now allow borrowers to digitally self-serve. They are guided through intuitive online questionnaires that automatically generate the fully compliant 1003 form in a matter of minutes.

Q3. Is there a difference between the Fannie Mae 1003 and Freddie Mac Form 65?

No, there is absolutely no difference between the two. They are the exact same standardized document, officially known in the mortgage industry as the Uniform Residential Loan Application (URLA). The different names simply reflect the two government-sponsored enterprises that mandate its use.

Q4. Do I need to pull credit before filling out a 1003?

You aren't strictly required to pull credit just to start the application. However, generating an accurate 1003, specifically the liabilities and debt sections, requires a hard credit pull. Today, AI tools automatically integrate this step, instantly importing the liabilities directly into the form.

Q5. How long does it take to fill out a 1003 form?

If done manually via PDF, a borrower can easily spend 30 to 60 minutes gathering documents and typing out answers. However, by leveraging modern AI-driven mortgage applications, borrowers can effortlessly finish the entire process in under 5 minutes.

Conclusion

The mortgage origination landscape has evolved dramatically. While the 1003 form remains a strict regulatory requirement for securing a home loan, how you choose to generate it dictates your long-term business success. Clinging to outdated PDFs or clunky, manual lender portals will only slow you down and cost you deals. It is time to embrace the future.

If you want to deliver 2.5x faster pre-qualifications and save yourself over 20 hours a month, I highly recommend upgrading your workflow with Zeitro's Application System today.

People Also Read

- Best Loan Origination Software for LOs/Brokers

- Best Mortgage CRM for Brokers, Lenders, MLOs

- Best AI Mortgage Underwriting Software for Loan Professionals

- Max LTV: Check Maximum Loan-to-Value Ratios By Loan Types

- Max DTI for Mortgage: Requirements By Loan Types