Written by

Eric

Share this article

.svg)

Subscribe to updates

As a mortgage professional, I know firsthand how exhausting the loan origination process can be. The constant battle of matching borrower profiles against hundreds of pages of complex investor rules is not just labor-intensive—it's a massive bottleneck. If you are searching for a way to quickly and accurately verify mortgage guidelines, you aren't alone.

We all need a reliable tool to stop wasting hours on manual underwriting. In this guide, I'll explain what a mortgage eligibility checker does and show you why leveraging an AI-powered assistant is the absolute best way to cut your research time down to literal seconds.

What is a Mortgage Eligibility Checker?

A mortgage eligibility checker is a specialized system that cross-references borrower data against vast investor guidelines to determine loan qualification. Historically, this meant flipping through massive PDFs or relying on clunky spreadsheets. Today, the most effective solution is a dedicated AI Agent.

After testing several platforms, my top recommendation for the US market is Zeitro. Founded in 2018 by engineering leaders from Google and Apple, it's an AI-native, completely neutral tech company with no lender affiliations. What gives me real peace of mind is their SOC 2 Type II certification, meaning your borrowers' sensitive data is protected by enterprise-grade security.

Their standout feature is Zeitro Strata AI, a wildly powerful guideline assistant. It uses a "DeepSearch" function to cross-check over 100 investors and 300+ guidelines simultaneously. Whether you are dealing with standard conventional loans or tricky Non-QM scenarios, like DSCR, ITIN, or Bank Statement loans, it delivers pinpoint accurate answers in seconds. Best of all, it provides exact source citations so you can confidently verify the information yourself. If a rule seems confusing, the "Explain" feature breaks it down further. You can even type your queries in multiple languages, including Chinese.

Beyond just guideline verification, Zeitro offers a complete ecosystem to streamline your entire workflow:

- GrowthHub: Lets you launch a personalized microsite to boost your SEO, display live rates, and capture organic leads.

- Digital 1003 (POS): Automates the borrower application, calculates DTI instantly with AI, and exports seamlessly in FNM 3.4 format.

- Pricing Engine: A real-time rate quote tool for both conventional and Non-QM products to help you offer competitive pricing on the spot.

Who is a Mortgage Eligibility Checker for?

In today's highly competitive housing market, the professional who delivers accurate pre-qualifications the fastest usually wins the deal. A robust eligibility checker is practically mandatory for anyone involved in loan origination.

Loan Officers & Brokers: If you interact directly with borrowers, this tool is a total game-changer. By automating the heavy lifting, you can deliver pre-qualifications 2.5 times faster and save over 7 hours per loan file. This frees you up to focus on relationship-building and bringing in new business.

Wholesalers & Lenders: For teams managing high volumes or complex lending criteria, eliminating 100% of manual guideline research is crucial. Using an AI system ensures an 85%+ income calculation accuracy, allowing your team to close loans up to 20% faster and ultimately increase your total closed loans by 30%.

Also Read:

- Best Mortgage CRM for Brokers, Lenders, MLOs

- Top Loan Origination Systems: Close More Loans Quicker

- [Proven] How to Generate Mortgage Leads for Free? 6 Methods

- Best Mortgage Loan Officer Training: Which to Pick?

- Best CRM for Loan Officers: Which One Suits You Most?

- How to Determine Mortgage Eligibility? Verify Guidelines in Seconds

How to Use a Mortgage Eligibility Checker?

Ditching the old method of manually hitting "CTRL+F" through endless PDFs is incredibly liberating. To show you how simple it is, here is how I use Zeitro Strata AI to check mortgage eligibility in my own daily workflow:

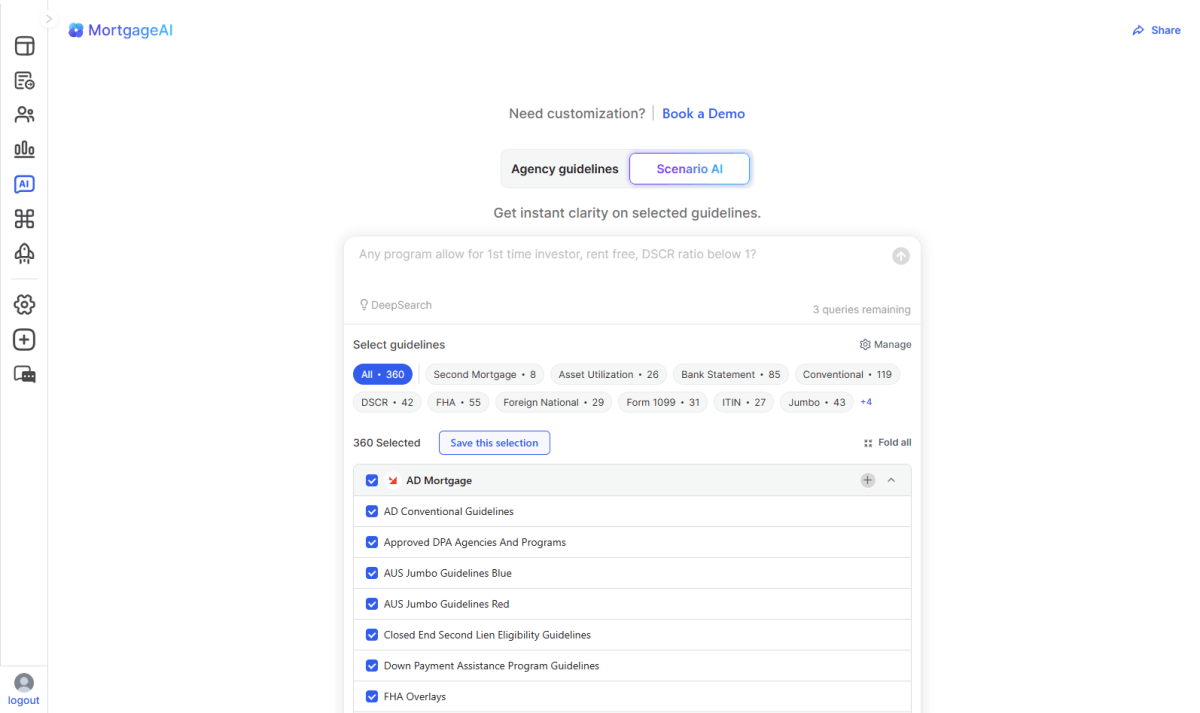

STEP 1. Input Your Scenario: Simply type your question into the chat interface. You can ask broad "what is" questions or highly specific eligibility queries. It even natively supports both English and Chinese inputs.

STEP 2. Customize Your Scope: Apply custom tags like DSCR, ITIN, loan-type, or specific investor names. This instantly narrows the DeepSearch to the exact programs you actually care about.

STEP 3. Get Instant, Sourced Answers: Within seconds, the AI provides a precise answer. I always click the provided citation link to double-check the source for 100% accuracy. If a specific caveat is unclear, I just use the "Explain" function for a deeper breakdown.

STEP 4. Share & Proceed: Once verified, you can easily share the results via a link or email to keep your clients and real estate partners perfectly in the loop.

FAQs About a Mortgage Eligibility Checker

Can an AI eligibility checker handle Non-QM loans?

Absolutely. In my experience, this is where a tool like Zeitro Strata AI truly shines. It continuously updates over 300 guidelines from major US lenders like AAA Lending, AD Mortgage, and AmWest, with deep support for complex Non-QM products like Profit and Loss, Foreign National, and DSCR loans.

Also Read: Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

How accurate are the AI-generated guideline answers?

They are highly accurate because the AI doesn't just guess or hallucinate. It actively cross-checks the most up-to-date guidelines and provides exact citations. You can always trace the answer back to the original source document, which virtually eliminates human error.

How much does a mortgage eligibility checker cost?

Pricing is surprisingly accessible. Zeitro offers a Freemium model. Their popular Explorer plan is completely free, giving you 3 queries per day, a personal website, and 10 lifetime FNM 1003 exports. For power users, it's just $8/month per user or $35/month per company.

Is my borrowers' data secure?

Yes. Security is a non-negotiable top priority in our industry. Zeitro is SOC 2 Type II certified. This means they maintain strict, enterprise-grade operational controls, ensuring all your sensitive customer data is fully protected from start to finish.

Final Word

Navigating the complexities of the US mortgage market shouldn't mean drowning in endless paperwork. A reliable mortgage eligibility checker is no longer just a luxury. It's an absolute necessity for modern loan professionals who want to scale their business. By adopting an AI Agent like Zeitro Strata AI, you can drastically improve your client satisfaction, speed up the lending process, and see a real boost in your overall ROI.

If you are tired of wasting hours on manual guideline research and want to close loans faster, it is time to make a change. I highly recommend taking advantage of Zeitro's Free Explorer Plan. You get three free queries every single day. So go ahead, test a complex scenario, and experience the magic of instant, accurate guideline verification for yourself.

![[2026 Guide] How to Calculate DTI Ratio for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69ccbafbc45f9a7b4a756616_how-to-calculate-dti-ratio-banner.png)