Written by

Eric

Share this article

.svg)

Subscribe to updates

As loan officers, we all know the headache of qualifying a borrower with rental properties. Between changing agency guidelines and messy tax returns, calculating rental income can feel like solving a puzzle with missing pieces. In my years of originating, I have watched underwriter guidelines shift constantly.

Today, we have two paths: grinding through complex worksheets manually, or using the Zeitro Rental Income Calculator to simply upload documents and let automation do the heavy lifting.

Key Takeaways

- Two Calculation Methods: Loan officers can manually compute rental income using IRS forms or leverage AI tools for speed.

- The 75% Rule: When using a lease agreement or market rent estimate for qualifying purposes, lenders typically count 75% of gross rent to account for vacancy, maintenance, and management expenses.

- Documentation is Key: Standard transactions demand tax returns, Schedule E, or current lease agreements backed by market rent studies.

What is Rental Income for a Mortgage?

In the mortgage industry, rental income is not just the monthly check our borrowers collect. For underwriting purposes, we must calculate the net qualifying rental income, which directly impacts the debt-to-income (DTI) ratio. Under Fannie Mae and Freddie Mac guidelines, we cannot simply use gross rent. Instead, we have to adjust the income to account for vacancies and operational costs.

Whether we are analyzing a subject property or a non-subject investment property, we look at the historical numbers on IRS Form 1040 Schedule E or current lease agreements. Understanding this distinction prevents us from over-promising loan approval amounts to our self-employed or investor clients.

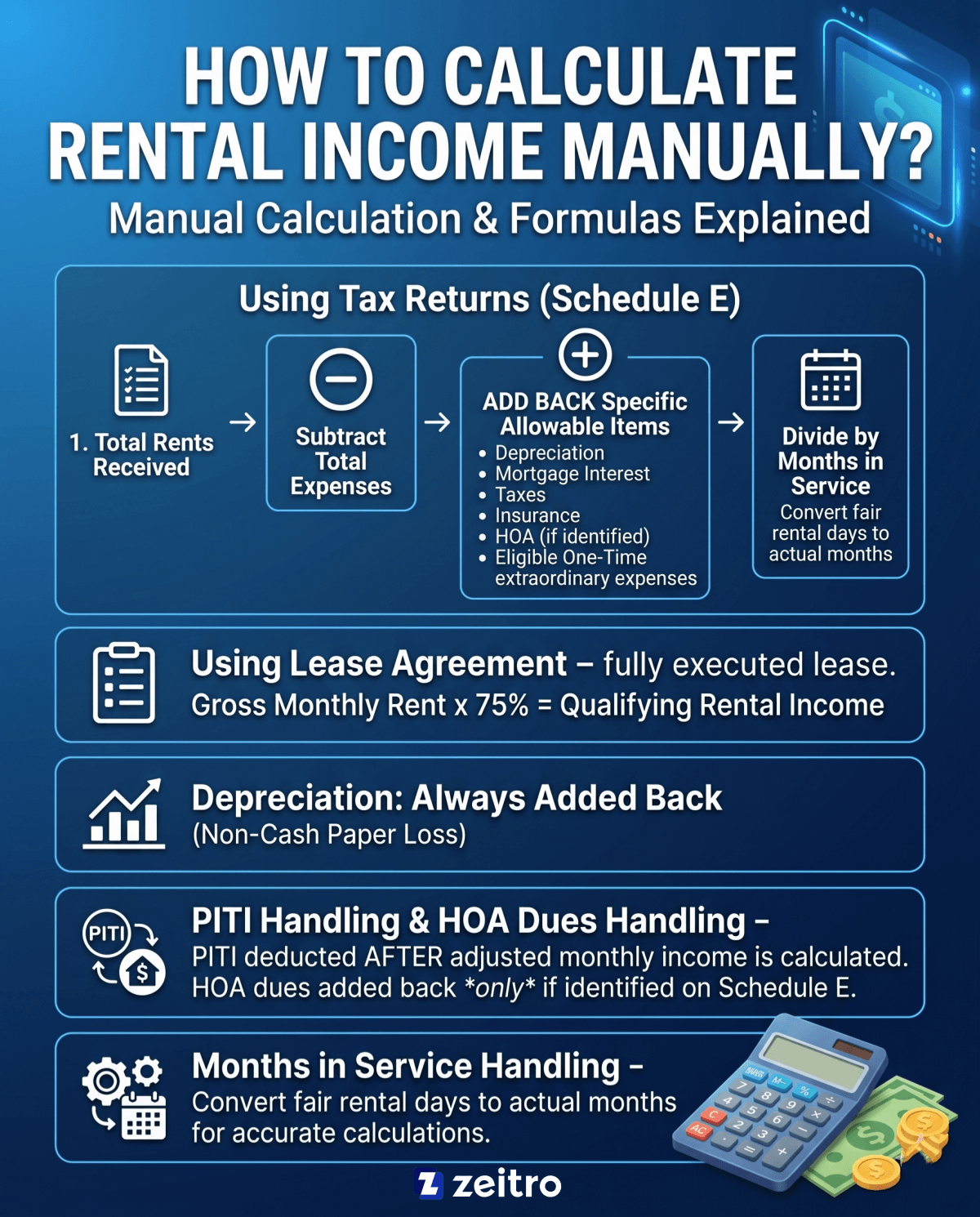

How to Calculate Rental Income Manually?

Calculating rental income manually requires dissecting the IRS Schedule E or adjusting a new lease agreement. When using tax returns, we analyze the net income or loss and add back non-cash expenses. The standard manual formula according to Fannie Mae is:

Schedule E income should be calculated by starting with total rents received, subtracting total expenses, adding back allowable items such as insurance, mortgage interest, taxes, HOA dues, depreciation, and eligible one-time extraordinary expenses, then dividing by the months in service before subtracting PITIA.

If the borrower has no tax history for the property, we use a fully executed lease agreement adjusted by a 25% vacancy factor:

Gross Monthly Rent x 75% = Qualifying Rental Income

To compute this accurately, we must understand these crucial parameters:

- Depreciation: Always added back since it is a non-cash paper loss.

- PITI/HOA: PITIA is deducted after calculating adjusted monthly rental income, and HOA dues may be added back only if they are specifically identified on Schedule E.

- Months in Service: Converting fair rental days to actual months ensures we do not artificially dilute the qualifying income.

How to Calculate Rental Income Easily and Smartly?

Over my career, manual math is where most processing delays happen. That is why I shifted to the Zeitro Rental Income Calculator. By simply uploading tax returns or lease agreements, the system automatically parses the data, drastically reducing human math errors.

What makes this tool incredibly powerful is that it is backed by Zeitro Strata, an AI-driven mortgage guideline assistant. Instead of spending 30 minutes digging through massive, outdated PDF guidelines from various lenders, we can run a deep search across over 100 investors in seconds. Zeitro Strata covers more than 1,000 guidelines, including conventional, Non-QM, and DSCR programs. The system provides 100% citation-backed answers, meaning we can instantly verify source guidelines and trace them back to specific lender sheets, eliminating AI hallucinations.

Whether we need to verify ADU rental rules, check AMI limits, or match local Down Payment Assistance programs, this platform handles it instantly. Best of all, we get 10 free queries daily to lookup rates and eligibility, helping us deliver fast, accurate answers that elevate our customer service.

Documents Required to Calculate Rental Income

Before we can run any calculations, collecting the right paperwork is the absolute first step. Underwriters are highly meticulous about document continuity, and missing pieces will quickly stall your loan in processing. To ensure a smooth approval process, we must gather the following documents from the borrower:

- IRS Form 1040, Schedule E: The borrower should provide the documents required for the specific scenario, which may include Schedule E tax returns, a current fully executed lease, and/or appraiser-supported market rent forms depending on the loan type and property situation.

- Current Signed Lease Agreements: Necessary if the property was recently acquired or has fresh tenants.

- Fannie Mae Form 1007 or Freddie Mac Form 216: Single-family comparable rent schedules completed by the appraiser to support lease terms.

FAQs About Rental Income Calculation

Q1. What is the formula for rental income?

The standard formula relies on your documentation. If using tax returns, we take the Schedule E net income, add back depreciation, interest, taxes, and insurance, and divide by the months in service. For new rental properties without tax history, we multiply the gross monthly rent on the signed lease agreement by 75% to account for a standard 25% vacancy and maintenance adjustment.

Q2. What is the best way to calculate rental income?

While manual calculation works for simple files, combining automated software with a reliable guideline database is the modern standard. Using a dedicated rental income calculator cuts down on calculation slips, while an AI assistant verifies investor overlays instantly. This hybrid approach ensures you remain compliant with both agency guidelines and specific Non-QM investor rules without wasting precious processing hours.

Q3. How does the 75% rule work in rental income calculations?

Lenders apply a 25% reduction to gross lease amounts to guard against potential vacancies and ongoing property upkeep costs. This means only 75% of the gross rent is counted as qualifying income. For example, if a property rents for $2,000 monthly, we can only utilize $1,500 to offset the mortgage payment or count toward the borrower's qualifying income.

Q4. Can you use rental income from a departing primary residence?

Yes, but guidelines differ based on landlord history. For departing or recently converted properties, the treatment of positive net rental income depends on the applicable investor guideline. Freddie Mac generally limits the income to offsetting PITIA unless the borrower has at least one year of investment property management experience, while Fannie Mae has its own separate rental income methodology.

Q5. What is the difference between QM and Non-QM rental income guidelines?

Qualified Mortgage guidelines generally follow standardized documentation and income-calculation rules, but the exact rental-income requirements vary by investor, property type, and transaction scenario. Non-QM programs, particularly Debt Service Coverage Ratio (DSCR) loans, focus primarily on the property's cash flow rather than personal tax returns. They determine qualifying income by comparing the gross rental income directly against the monthly housing payment, ignoring personal debt-to-income ratios entirely.

Final Word

In our industry, timing and accuracy are everything. A miscalculated debt-to-income ratio can turn a pre-approval into a denied loan at the underwriting desk, damaging our professional relationships and reputations. Mastering the manual calculations gives us a strong foundational understanding, but our daily focus must be on speed and compliance.

I highly recommend checking out the Zeitro Rental Income Calculator to simplify your daily pipeline. Combining automated calculations with Zeitro Strata allows us to close loans faster, answer guidelines with confidence, and free up our calendars to focus on what we do best—originating.

People Also Read

- How to Calculate Self-Employed Income for a Mortgage?

- How to Calculate Employment Income for a Mortgage?

- Mortgage Income Requirements: Learn Before You Apply

- How to Verify Income for Mortgage: Detailed Guide for Loan Pros

- Income Verification Documents: A Complete Guide for Employees and Self-Employed