![[Solved] How Much Interest Will I Pay on My Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a0d2c55ec69e0e25bff099e_how-much-interest-will-i-pay-on-my-mortgage-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

When I first bought a house, I was absolutely shocked to see the total interest I'd be handing over to the bank—it felt like buying a second home! Buying property is likely your biggest life expense, but have you actually calculated the true cost? In this guide, we'll dive into exactly how to figure out the interest on your mortgage and share real strategies to minimize it using a mortgage calculator with interest.

Key Takeaways

- Interest often makes up a massive portion of your total repayment, sometimes rivaling the principal amount itself.

- The fastest, most accurate way to check your numbers is by using an online mortgage calculator.

- Your interest rate, loan term, and down payment are the core factors dictating your overall borrowing costs.

Why Does Interest Matter in a Mortgage?

Interest isn't just the basic cost of borrowing money. It's a financial force that can dramatically inflate your home's purchase price. For example, on a 30-year loan at a 6.5% interest rate, your total interest paid can sometimes exceed the original amount you borrowed, especially with higher interest rates and longer loan terms. Here is why you absolutely must pay attention to it:

- True Cost of Homeownership: It determines what you actually pay for the house over the decades, far beyond the sticker price.

- Monthly Budget: Higher interest means steeper monthly payments, directly impacting your everyday cash flow.

- Equity Building: In the early years of repayment, a large portion of your monthly payment goes toward interest rather than principal.

Methods to Estimate How Much Interest to Be Paid

There are generally two paths you can take to figure out your future housing costs: leveraging a modern digital tool or crunching the numbers yourself using traditional math. Let's break down both options.

Fastest Way: Use an Online Mortgage Calculator

If you want to avoid math anxiety, the absolute best method is using a digital tool like the Zeitro Mortgage Calculator. You simply punch in your home price, down payment, and interest rate. In under five seconds, it generates precise results.

What I love most about this specific tool is its visual "Amortization Breakdown." It clearly contrasts your remaining principal, paid principal, and paid interest over the loan's lifetime. It even isolates the Total Interest Over Loan Lifetime so there are no surprises.

Pros: It's 100% free, provides instant visual charts, prevents human math errors, and can factor in hidden costs like HOA fees and property taxes.

Cons: The numbers are estimates. Your final, locked-in rate will ultimately depend on your official loan professional.

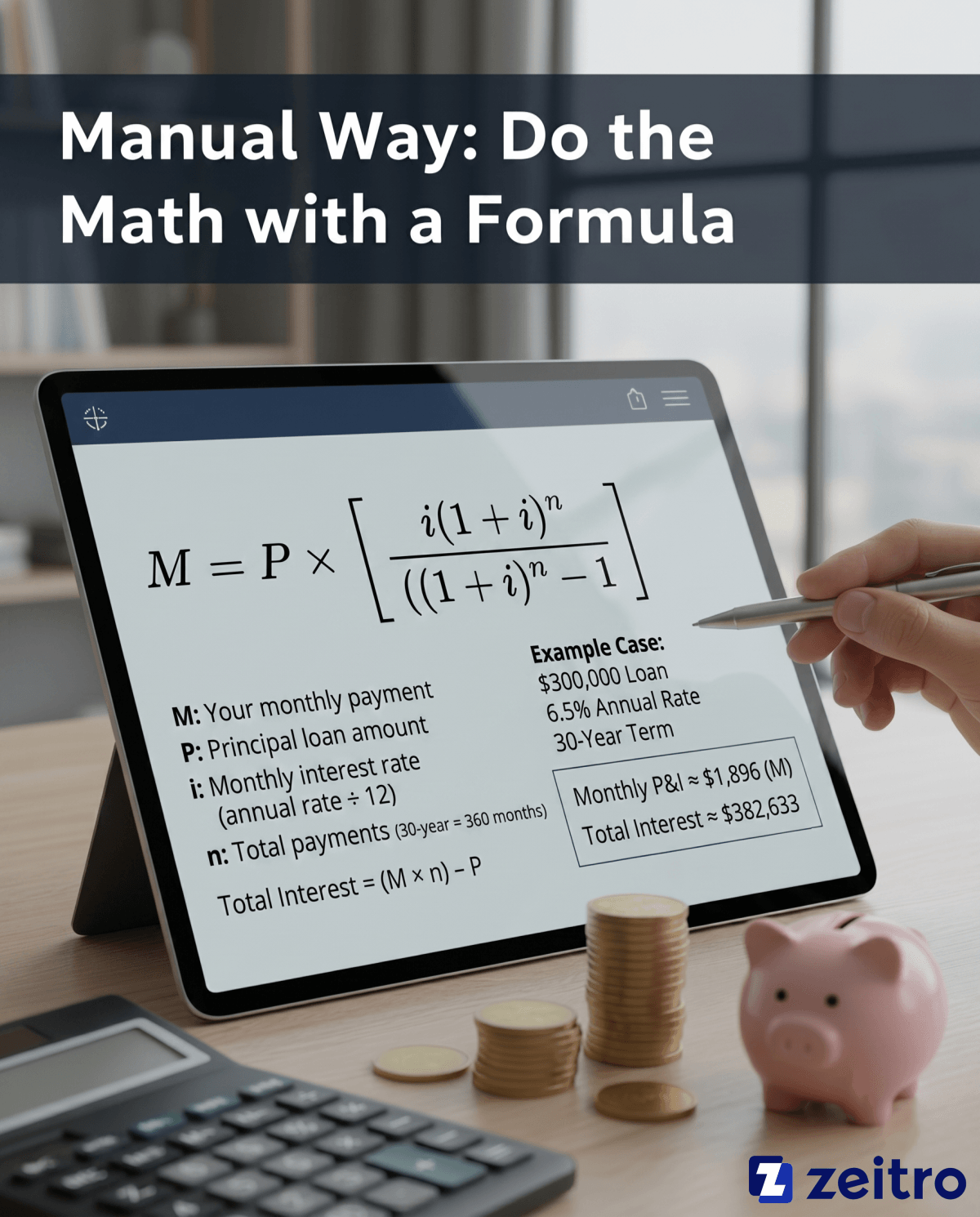

Manual Way: Do the Math with a Formula

For those who love crunching numbers, you can calculate the exact interest manually using the standard industry formula for monthly payments: M = P × [ i(1 + i)ⁿ / ( (1 + i)ⁿ − 1 ) ].

Here is what the variables mean:

- M: Your monthly payment.

- P: Principal loan amount.

- i: Monthly interest rate (annual rate divided by 12).

- n: Total number of payments (a 30-year loan equals 360 months).

Once you find M, your total interest is simply (M × n) - P.

For example, if you borrow $300,000 at a 6.5% rate for 30 years, your monthly principal and interest is roughly $1,896. Over 360 months, you will pay about $382,633 in pure interest! This complex math is exactly why digital calculators are so handy.

Comparison Between Two Methods

While both approaches eventually lead you to the same financial truth, the user experience couldn't be more different.

- Speed & Convenience: An online calculator gives you instant answers and lets you seamlessly tweak variables, like changing your down payment from 10% to 20%. Manual equations take time, and a single misplaced decimal ruins the whole calculation.

- Comprehensiveness: The digital tool integrates realistic monthly burdens, like Private Mortgage Insurance (PMI), local property taxes, and homeowners association fees. The math formula only isolates pure principal and interest.

- Visualization: Calculators provide a dynamic amortization curve so you can literally see when your payments shift from interest-heavy to principal-heavy. Hand-written math leaves you blind to that timeline.

Knowing the formula builds your financial literacy, but the digital calculator is the undisputed winner for practical planning.

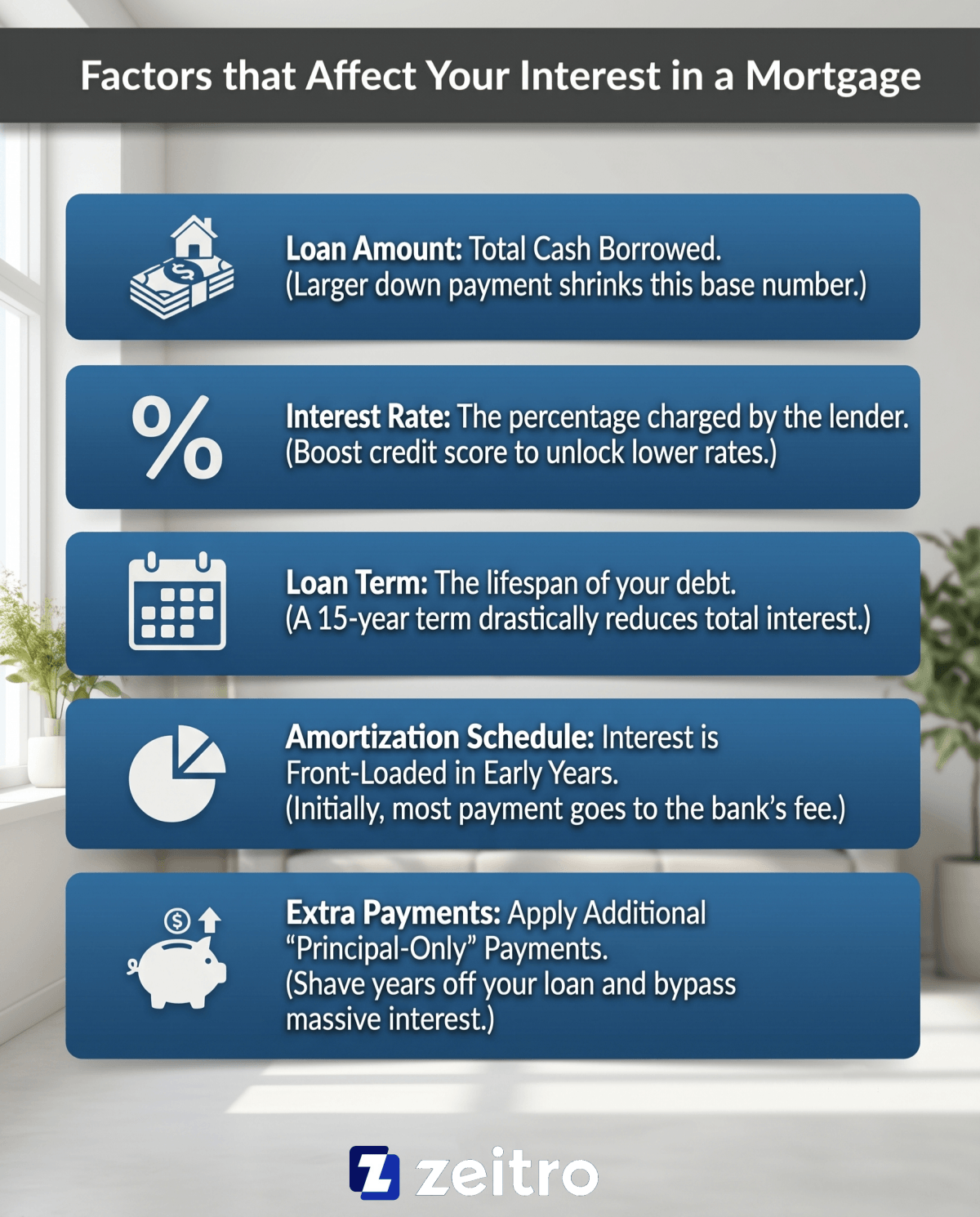

Factors that Affect Your Interest in a Mortgage

Your final interest bill isn't completely at the mercy of the market. Several elements are within your control:

- Loan Amount: The total cash you borrow. A larger down payment shrinks this base number and can even eliminate costly PMI.

- Interest Rate: The percentage charged by the lender. Boosting your credit score is the single best way to unlock lower rates.

- Loan Term: The lifespan of your debt. A 15-year term means higher monthly bills but slashes your total interest by tens of thousands of dollars.

- Amortization Schedule: Lenders front-load interest. In the early years, you're mostly paying the bank's fee rather than buying your house.

- Extra Payments: Committing to just one extra "principal-only" payment each year can shave years off your loan and help you bypass massive amounts of interest.

FAQs About How Much Interest Will I Pay on My Mortgage

Q1. How to calculate how much of a mortgage payment is interest?

Your first month's interest is simply your remaining loan balance multiplied by your monthly interest rate. Because loans are amortized, the interest portion shrinks slightly every single month as your principal balance goes down, shifting more money toward your home equity.

Q2. Can I reduce the total interest on my current mortgage?

Absolutely. You can set up bi-weekly payments (resulting in one extra full payment per year), throw annual work bonuses directly at the principal balance, or refinance into a lower rate or a shorter loan term when market conditions improve.

Q3. Is the interest on my mortgage tax-deductible?

Yes, in the US, you can often deduct this cost if you itemize your taxes. As of current U.S. tax law, the mortgage interest deduction limit is set at $750,000 of mortgage debt for married couples filing jointly, though this provision may change depending on future legislation. Always consult a certified tax advisor for personalized guidance.

Q4. Why is my total interest sometimes higher than my loan amount?

This is the result of long-term amortized interest, where interest is calculated on the remaining loan balance over time. When you spread payments over 30 years, especially during periods when average rates sit around 6% or 7%, the accrued interest slowly snowballs until it eclipses your original purchase price.

Q5. Does a 15-year mortgage really save me money on interest?

Yes, significantly! Because you are paying the debt off in half the time, and 15-year loans typically offer lower interest rates to begin with, your total interest paid is typically significantly lower than with a 30-year mortgage, sometimes by more than half, depending on the rate and terms.

Conclusion

Understanding how mortgage interest works is your first step toward brilliant financial decisions. The numbers might look intimidating at first, but you have the power to control them. By saving for a larger down payment, boosting your credit score, or making extra principal payments, you keep more money in your pocket over the long haul.

Don't just guess your future expenses. I highly encourage you to use the Zeitro Mortgage Calculator today. Plug in your budget, see the real data, and plan your homeownership journey with absolute confidence!

Disclaimer: The formulas, tools, and tax limits mentioned in this article are for estimation and educational purposes only. Always consult a licensed loan professional and tax advisor to confirm your exact rates and specific financial details.

People Also Read

- Zeitro Mortgage Affordability Calculator Free and Online

- [Solved] How Much Will My Monthly Payment Be?

- Must-Read Tips for Paying Off Mortgage Early in 2026

- Gross vs. Net Income for a Mortgage: What Lenders Use & Why

- [Solved] At What Income Level Do You Lose Mortgage Interest Deduction?

![[Solved] How Much Will My Monthly Payment Be?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a0a8b1f89bcb9d995d94157_how-much-will-my-monthly-payment-be-banner.png)