Written by

Eric

Share this article

.svg)

Subscribe to updates

I've been there. You find the perfect investment property, the numbers look incredible, but then your CPA reminds you that you wrote off so much income last year that you look “broke” on paper. It's the classic real estate investor's dilemma: smart tax planning often destroys your ability to qualify for a conventional mortgage.

That is exactly where a DSCR (Debt Service Coverage Ratio) loan saves the day. Unlike traditional financing, a DSCR loan doesn't care about your W-2s or tax returns. It cares about one thing: Does the property generate enough rent to pay for itself?

In 2026, lenders have tightened some guidelines while loosening others, particularly for short-term rentals. In this guide, I'm going to walk you through the exact requirements you need to hit this year to get approved, so you can stop worrying about DTI (Debt-to-Income) ratios and start scaling your portfolio.

Quick Summary: DSCR Loan Requirements at a Glance

If you are in a rush and just need the raw numbers to see if you qualify, here is the snapshot of the current lending landscape.

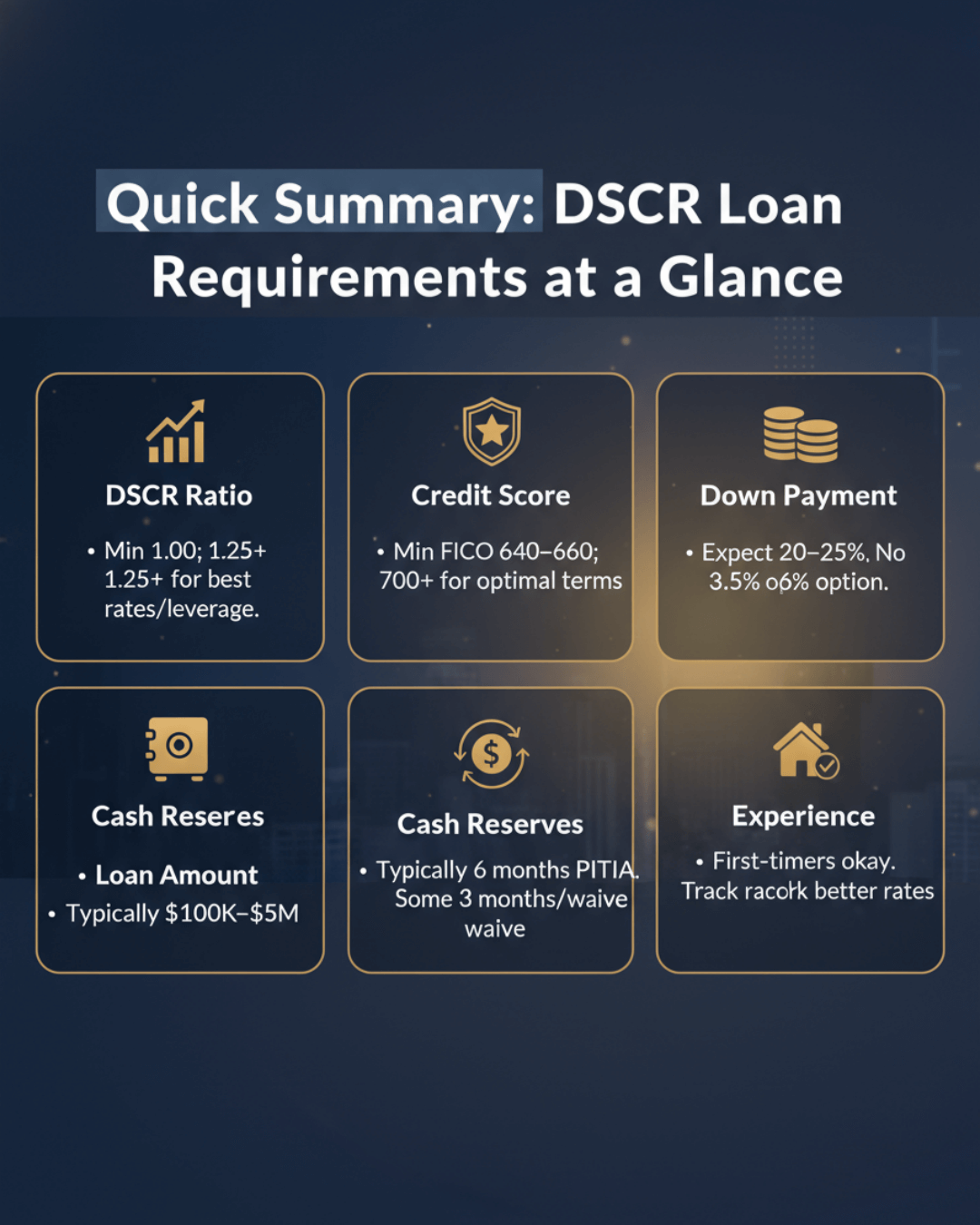

To qualify for a DSCR loan in 2026, lenders typically look for the following criteria:

- DSCR Ratio: Lenders typically require a minimum DSCR of 1.00 or higher, with 1.25+ unlocking the lowest rates and maximum leverage.

- Credit Score: Expect a minimum FICO of 640–660, with scores above 700 needed for optimal terms and higher LTV.

- Down Payment: Expect to put down 20% to 25%. Unlike FHA loans, there is no 3.5% down option here.

- Cash Reserves: Lenders typically require 6 months of PITIA payments in liquid reserves post-closing, though some accept 3 months or waive for cash-out refinances.

- Loan Amount: Typically start at $100,000–$150,000 and reach up to $3–5 million for qualifying properties.

- Experience: While "first-time investors" can qualify, having a track record of owning at least one other property often unlocks better rates.

Minimum DSCR Ratio Lenders Look For

The "Ratio" is the heart of this loan. If you understand this math, you understand how to get approved.

The formula lenders use is simple: DSCR = Gross Rental Income ÷ Total Monthly Debt (PITIA)

PITIA includes Principal, Interest, Taxes, Insurance, and HOA fees.

DSCR lenders price your loan based on risk tiers. Here is what I am seeing in the market right now:

- The Safe Zone (> 1.25): If your rent is $2,500 and your mortgage is $2,000, your ratio is 1.25. This gets you the lowest interest rates and easiest underwriting.

- The Break-Even Zone (1.00 – 1.24): The property pays for itself, but barely. You can still get funded, but the rate will be slightly higher.

- The No-Ratio Zone (< 1.00): Yes, you can get a loan even if the property loses money monthly (often used for properties in high-appreciation areas like Austin or Miami). However, expect to put 30-35% down and pay a significantly higher rate.

If your ratio is tight (e.g., 0.95), consider buying down the interest rate with "points." Lowering the rate lowers the monthly payment, which mathematically raises your DSCR ratio back into the passing zone.

Credit Score & Borrower Qualifications for DSCR Loans

A common misconception I hear is, "Since they don't look at my income, my credit score doesn't matter." False. In fact, because they aren't looking at your income, your credit history is the primary way lenders judge your reliability.

While the technical minimum score is often 620, I wouldn't recommend applying with that score unless you have no other choice. Lenders use a tiered pricing matrix:

- 740+ FICO: Unlocks the maximum LTV (up to 80%) and the lowest rates.

- 700–739 FICO: Standard rates, usually 75% LTV max.

- 620–679 FICO: You will likely be capped at 65% or 70% LTV, meaning you need a larger down payment, and your rate could be 1–2% higher than a top-tier borrower.

If you have had a bankruptcy or foreclosure, you typically need to wait 3 to 4 years before applying. This is much shorter than the 7-year wait for conventional loans, which is a huge advantage for investors recovering from a rough patch.

Also, I highly recommend closing these loans in an LLC (Limited Liability Company). Closing in an LLC is common and preferred by many lenders for asset protection, though personal guarantees may still apply.

Down Payment, LTV, and Reserve Requirements

Let's talk cash to close. DSCR loans are commercial-grade products, so they require "skin in the game."

In 2026, the standard down payment is 20% for a purchase. If you want a slightly better rate, 25% is the sweet spot.

- Purchase: Max 80% LTV (Loan-to-Value).

- Cash-Out Refinance: Max 70% – 75% LTV. Lenders are more conservative when you are pulling cash out.

This is where many beginners get denied. You cannot drain your bank account to zero at the closing table. Lenders require Reserves, liquid cash left over after the down payment.

- Requirement: Usually 6 months of PITIA payments.

- Example: If your mortgage is $2,000/month, you need $12,000 sitting in the bank after you pay the down payment.

- Acceptable Sources: Business bank accounts, personal savings, and sometimes stocks/401k (though they may only count 70% of the vested value).

- If you are short on cash, some lenders allow Gift Funds from a family member, but verify this early, not all DSCR lenders allow gifts.

Eligible Property Types & Loan Product Variations

One of the biggest shifts in 2026 is how lenders view Short-Term Rentals (STRs). A few years ago, financing an Airbnb with a DSCR loan was tough. Now, it's a standard product.

Eligible property types include the following.

- Standard: Single-Family Homes (SFR), Condos, Townhomes.

- Small Multi-Family: 2–4 Unit properties (Duplex, Triplex, Fourplex).

- Large Multi-Family: 5+ units usually fall under commercial multifamily loans, not residential DSCR.

If you are buying a vacation rental, you don't have a long-term lease to show the lender. Lenders now accept data from AirDNA or a 1007 Rent Schedule marked for short-term usage. Lenders will often cut the projected AirDNA income by 10-20% to be safe. Ensure your numbers still work with that "haircut."

To maximize cash flow, many investors look for Interest-Only DSCR loans. You only pay interest for the first 10 years. This lowers your monthly obligation significantly, which boosts your DSCR ratio and puts more cash in your pocket today, though you aren't paying down principal.

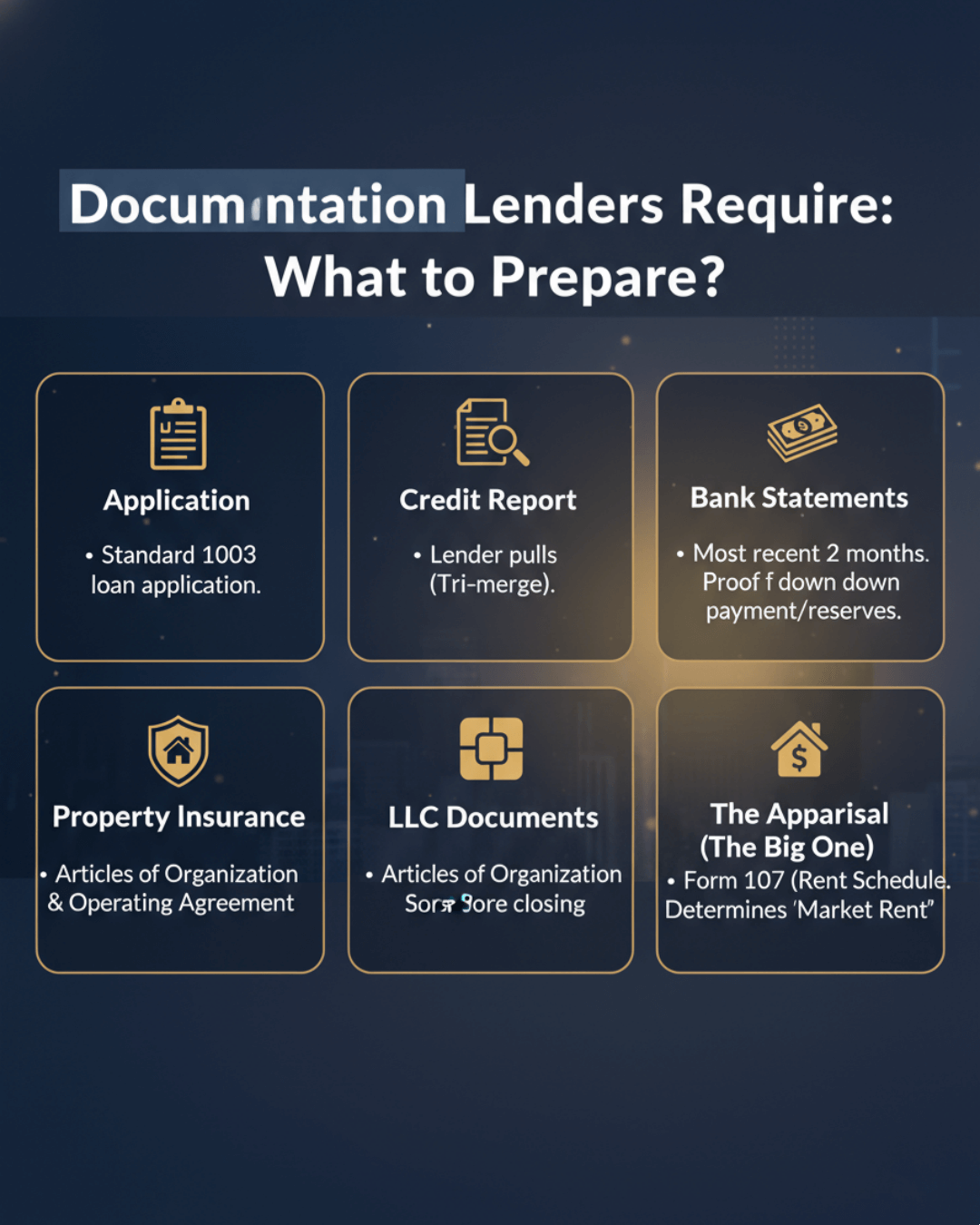

Documentation Lenders Require: What to Prepare?

The beauty of this loan is the lack of paperwork. You can skip the call to your accountant. However, "Low-Doc" doesn't mean "No-Doc."

Here is the checklist you need to have ready:

- Application: Standard 1003 loan application.

- Credit Report: The lender will pull this (Tri-merge).

- Bank Statements: Usually the most recent 2 months to prove you have the down payment and reserves.

- Property Insurance: You need a policy ready before closing.

- LLC Documents: Articles of Organization and Operating Agreement.

- The Appraisal (The Big One): The appraiser fills out a Form 1007 (Rent Schedule). This document tells the lender what the "Market Rent" is. If the appraiser says the rent is $2,000, but you think it's $2,500, the lender uses the appraiser's number. This can kill your ratio. Meet the appraiser at the property with comps in hand to justify your rental numbers!

How to Qualify: 6 Practical Steps to Improve Approval Odds

Navigating the Non-QM (Non-Qualified Mortgage) world can be tricky because every lender has different rules. Here is my proven workflow to get from application to funding.

- Check Your Credit: Ensure you are above 700 if possible. If you are at 660, pay down some credit card balances to boost your score before applying.

- Calculate Your Own DSCR: Don't guess. Take the expected rent and divide it by the new mortgage payment (including taxes/insurance). If you are under 1.15, you might need to put more money down.

- Organize Your Entity: Have your LLC registered and your EIN ready. Lenders hate waiting on state paperwork.

- Shop and Compare Rates (Critical Step): Here is the secret: DSCR rates are not standardized like conventional mortgages. Lender A might quote you 7.5% while Lender B quotes 8.5% for the exact same deal. That 1% difference kills your cash flow. I strongly recommend comparing quotes from multiple specialized loan officers. You can do this easily at Bluerate.

- Order the Appraisal: Once you pick a lender, they order the appraisal. Pray for a good rental valuation.

- Close: Sign the docs, wire the funds, and pick up the keys.

Common DSCR Loan Requirements FAQs

Q1. Do DSCR loans typically require 20% down?

Yes. 20% is the industry standard minimum. While you might find a rare lender offering 15% down in a booming market, it usually requires an 800+ credit score and comes with a punishingly high interest rate.

Q2. Can equity be used for a DSCR down payment?

Yes. If you own another property with high equity, you can do a "Cash-Out Refinance" on that property first to generate the cash for the DSCR down payment. Some lenders also allow "Cross-Collateralization" loans, where you pledge two properties to secure one loan.

Q3. Is it difficult to qualify for a DSCR loan?

No, generally it is easier. Because there is no income verification or DTI calculation, the process is faster and less invasive than a conventional loan. If you have the cash for the down payment and a decent credit score, you will likely qualify.

Q4. What are the downsides of DSCR loans?

The main downsides are Rates and Prepayment Penalties. Expect an interest rate 1%–2% higher than a standard conventional loan. Also, most DSCR loans have a "Prepayment Penalty" (e.g., a 5-year step-down), meaning if you sell or refinance quickly, you pay a hefty fee.

Q5. How long are DSCR loan terms available for?

30 Years is standard. Most are 30-year fixed loans. However, 5/1 ARMs (Adjustable Rate Mortgages) and 40-year Interest-Only terms are also available if you need lower monthly payments to make the cash flow work.

Conclusion: Is a DSCR Loan Right for Your Investment?

In the 2026 real estate market, agility is everything. If you are a self-employed investor, or if you simply want to keep your personal debt-to-income ratio clean for a future primary home purchase, the DSCR loan is arguably the best tool in your arsenal.

Yes, the rate is slightly higher, and you need a solid down payment. But the ability to scale your portfolio without handing over your tax returns is a superpower.

If you are ready to see what numbers you can qualify for, don't just take the first offer you get. Compare live quotes. It's the smartest way to ensure your new investment starts profitable from day one.

People Also Read

- Are Mortgage Rates Expected to Go Down in 2026? Expert Forecasts

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

- 6 Best Loan Origination Software for LOs/Brokers

- Detailed Guide: How to Become a Loan Officer with No Experience?